Your mortgage is almost paid off, the kids have started leaving the nest, and now you have some spare cash.

But before you retire, you’d also like to change jobs, maybe help the children, and do some travelling before it’s ‘too late’…without affecting your retirement savings.

And when you do finally pull up stumps, you want to know you can turn the air-con on, take the grandkids on a sneaky trip to the shops, and enjoy a delicious Sunday roast (instead of two-minute noodles) without sweating the cost.

And then when you want to escape it all, you want to know you can jump on a plane and say, “hello to the golden beaches of the Caribbean (and good riddance to another miserable winter)”.

But most of all, you want to know how much you need to retire without taking a big drop in living standards. You’ve worked too hard for that!

There is no doubt in my mind that financial planning is just like farming. And that’s why here in Balmain, when you come to see us, you can expect something very different…in case it wasn’t already obvious to you.

(By the way, we don’t wear suits).

We take you through a process called ‘Growing Your Financial Farm…one paddock at a time’.

Meaning, just like a farmer doesn’t try and work on every paddock at once, we take the same approach with your finances. We prioritise your dreams and goals depending on your season, or ‘life stage’ and work from there. In other words, we sow and reap one paddock at a time.

Make sense?

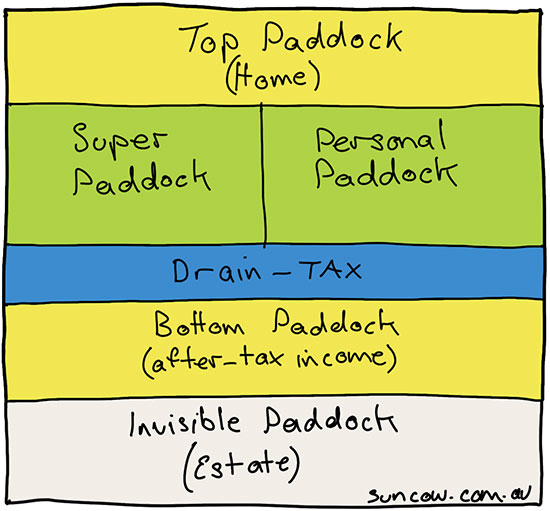

And in case you’re wondering what your financial farm looks like, here it is. It’s what we call…

At Suncow, we break your financial farm up into five paddocks to make growing your money very easy to understand. This is what they look like…

Your Top Paddock is your home. Therefore, your first goal when growing your farm should be to pay off your mortgage as soon as possible and get rid of your ‘non-deductible’ debt.

And then we have…

Your Super and Personal Paddocks. These are your two wealth building paddocks. They are also the two paddocks we focus on most to grow your money in preparation for your retirement.

BTW…your personal paddock can include structures such as trusts and stuff, but ultimately, you still only have two paddocks (super & personal) to grow your money.

Your Tax. This drain runs along the bottom of your two wealth building paddocks and if you’re not careful, your drain can do a lot of damage to…

Your Bottom Paddock. This is the most important paddock of all because its where your after-tax money lands. Therefore, your ultimate goal is to get as much money across the drain into your bottom paddock ready to fund your retirement. Make sense?

And finally, we have…

Your Invisible Paddock, otherwise known as your estate. We call it this because no-one see’s it come into reality until you’ve gone to God.

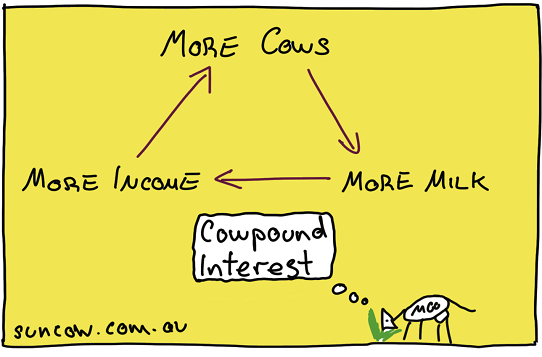

I constantly get asked, “what’s the best superfund?”.

The truth is super is just a tax-effective paddock. The only difference is what cows you put in your super paddock – beef cows (capital growth) or dairy cows (income).

To help plan for your retirement and make sure you have plenty of income, we recommend the dairy cow approach.

Meaning, suppose you have a herd of dairy cows and all you do is sell the milk to buy more dairy cows.

If you keep repeating the process, you begin to compound the size of your herd.

And that’s all you need to do with your super – cow-pound it. Just keep growing your herd until it’s time to retire and then live off the income.

BTW…do NOT sell your cows to fund your retirement. Less cows means less milk and less income.

And don’t worry about how much your herd (portfolio) is worth, just concentrate on how much milk (income) it produces.

If you focus on compounding the growth of your herd by reinvesting, you will never have to rely on the markets to grow your super. Nor will you be affected when the markets go down either.

Make sense?

This all sounds great but where do I start and how do I know I’m doing the right thing?

I understand, I hear that all the time.

And that’s why I recommend you begin with our One Page Financial Plan.

It’s a low-risk, low-cost way of getting started.

Most importantly, we’ll address your two most important questions…

How much do you need to retire and will you have enough?

The cost is a flat fee of $660 (inc gst).

Email me at adam@suncow.com.au or call 0418 785 200 to book your ninety-minute discovery meeting in Balmain, Sydney’s Inner West.

Information provided by Suncow Wealth is general in nature and does not take into consideration your personal financial situation. It is for educational purposes only and does not constitute formal financial advice. Remember, the value of any investment can go down as well as up. Before acting, you should consider seeking independent personal financial advice that is tailored to your needs. Suncow Wealth Pty Ltd is a Corporate Representative No.441116 of AFSL 342766.