Here’s a question most pre-retirees never get asked.

How much income will your money produce?

Not “how much super do you have?” Not “what’s your portfolio worth?” Not “have you hit the magic million yet?”

Because here’s the thing nobody in the financial industry seems particularly keen to tell you: your super balance is not your retirement income. Your net worth is not your retirement income. The number on your super fund dashboard at 11pm on a Sunday night when you can’t sleep — that is not your retirement income.

It’s just a number. And you can’t spend a number.

What you can spend is income. Regular, reliable cash that arrives in your account whether the market is having a good year or an absolute shocker. The kind of income that pays the electricity bill, funds the annual trip to see the grandkids, and covers a decent Sunday roast without you having to think twice about it.

That’s what retirement actually runs on. And it’s what most retirement strategies completely fail to plan for.

If you’ve spent any time Googling retirement planning, you’ll have noticed that everyone seems to have a number.

$1 million. $1.5 million. $2 million “if you want to be safe.” Some calculator on a super fund website that spat out a figure so terrifying you closed the tab and made a cup of tea.

The financial industry loves these numbers. Big, scary lump sums keep people anxious, engaged, and logging into their super dashboards. They’re great for business.

But they’re a lousy way to plan a retirement.

Because the question “how much super do I need?” is actually the wrong question. It focuses your attention entirely on a balance — a static figure — rather than on what that balance can actually do for you.

Think about it this way. If someone offered you a choice between $800,000 in a growth fund that produces almost no income, and $600,000 in a portfolio that generates $40,000 a year in reliable distributions — which one actually funds your retirement?

The $600,000. Every time.

Balance doesn’t pay your bills. Income does.

And the moment you shift from asking “how much do I have?” to asking “how much does it produce?” — everything about retirement planning changes.

Here’s what a genuine retirement income strategy looks like, stripped of the jargon.

You figure out how much income you actually need each year to live the life you want. Not some generic benchmark. Your life. Sunday roasts, decent holidays, grandkids at Taronga Zoo, the occasional indulgence that doesn’t require a spreadsheet to justify.

Then you build an asset base — inside super and outside it — that generates that income reliably, year after year, without requiring you to sell anything.

That last part is critical. The traditional approach to retirement is to accumulate capital, then gradually sell it down to fund your living costs. Build up the pile, then chip away at it. The goal, in this model, is to not run out before you die.

Which sounds fine in theory. But in practice it’s terrifying, because every year your buffer shrinks. Every market downturn forces you to recalculate your runway. Every spending decision becomes a question of how much of your capital you’re consuming. This is the financial architecture of FORO — the Fear of Running Out — and it’s built into the conventional retirement approach by design.

There’s a better way. And it came to me, of all places, from watching how farmers think.

Growing up, all I wanted to be was a farmer. That’s what my grandparents did, that’s how my parents started out, and it’s all I wanted to do.

Then the tractor made a hard left turn.

I went to uni, got a degree, and ended up becoming a stockbroker instead of a stockman. And while it might seem like I’m a long way from the farm, I’ve always reckoned that farming and finance are more alike than most people think.

Both require patience. Both require planning. Both are about nurturing growth over time rather than chasing quick wins. And both come down to one fundamental question: are you building something that produces, or something you just hope to sell at a profit?

That question nagged at me for years. And eventually it became the foundation of everything I do.

Same paddock. Different outcome.

Imagine you have 100 cows to fund your retirement.

You’ve got two ways to generate income from them. You can sell the milk they produce. Or you can sell a few cows each year.

Option two sounds reasonable — until you think it through. The price of cows fluctuates. You might need to sell in a bad year. Sell enough of them and eventually you run out. Which is exactly what most people are afraid of.

Option one is different. Milk the cows. Live off the income. Never touch the herd.

That’s the 2 Cows Strategy in a sentence. Build an asset base that produces reliable income. Live off that income. Never sell the herd.

But to really understand why this works — and why most people are doing the opposite without realising it — you need to understand the difference between two very different kinds of cow.

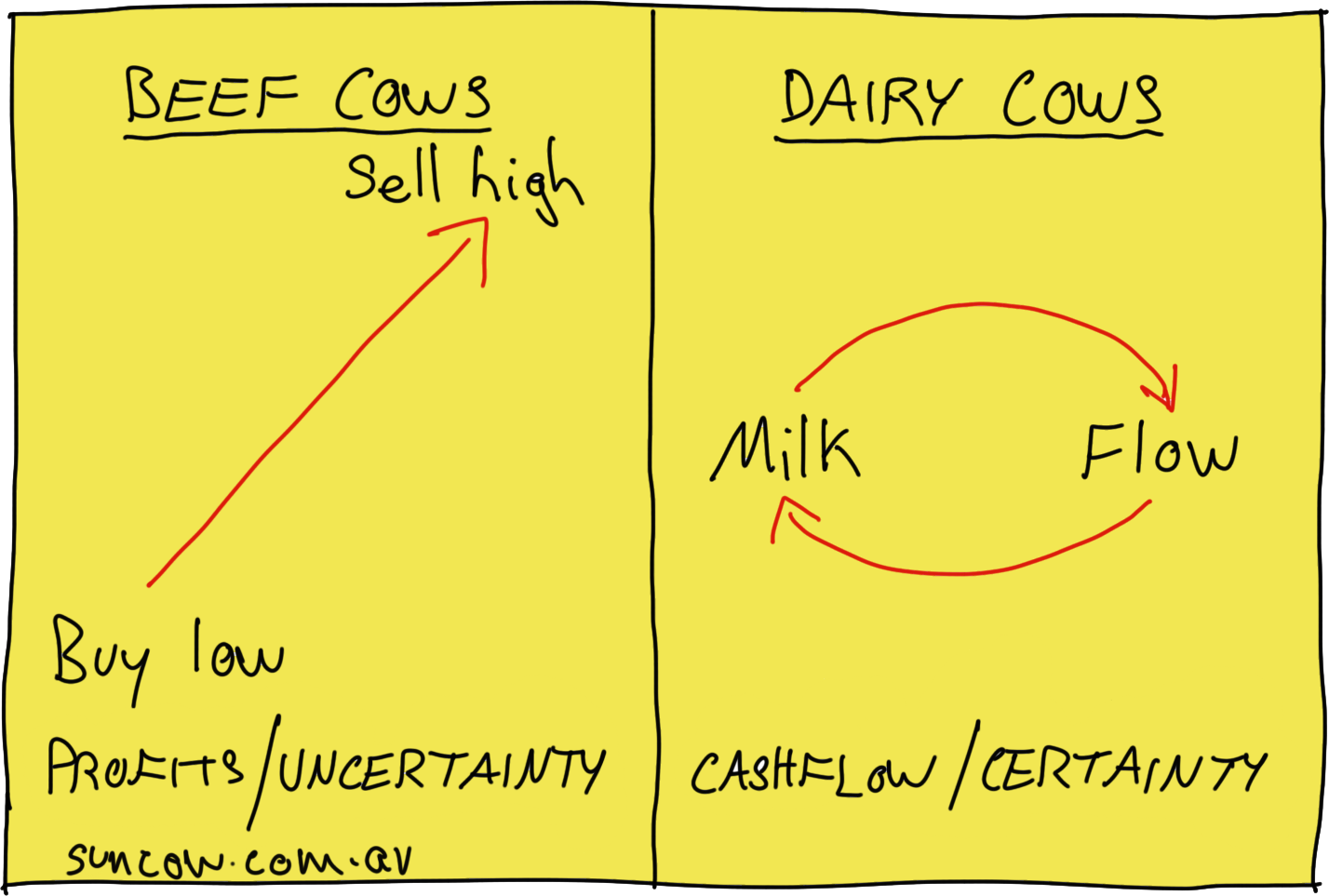

Beef Cattle — The Way Most People Invest

Suppose you’re a beef farmer. Your model for making money is simple: buy young calves cheap, grow them into bigger cattle, sell them at a profit. Buy at $200, sell at $1,000. The difference is your income.

The problem is you’re always at the mercy of the market. Cattle prices fluctuate. Seasons turn. Floods, drought, global commodity shocks — none of it is in your control. Your income depends entirely on selling at the right time, at the right price, into whatever market happens to exist that day.

Unfortunately, this is exactly how most Australians invest for retirement. Buy low, sell high. Hope the market cooperates. Gradually sell down the portfolio to fund living costs. The whole strategy depends on timing — and timing the market is a game that very few people win consistently.

It’s a beef cattle strategy. And it’s riddled with uncertainty.

Dairy Cattle — The Suncow Way

Now suppose you’re a dairy farmer instead.

Your model is completely different. You maintain a herd of dairy cows that get milked twice a day, 365 days a year. Their constant milk flow becomes your constant cashflow. When you wake up on January 1 every year, you know within close proximity how much milk your cows will produce — and therefore what your income will be for the year.

You’re not dependent on markets going up. You’re not selling anything. You’re just collecting what your herd produces.

This is the retirement income strategy we build at Suncow. An asset base that generates good, consistent cashflow — dividends, distributions, interest, rent — regardless of what markets are doing. Because the only way to truly beat FORO is to build retirement income strategies that don’t depend on selling anything.

Good question. And it’s the one I get asked most often.

Imagine a cow standing in a paddock, happily grazing, making milk. The next day, the market for cattle falls through the floor. Her value drops 30% overnight.

Do you think she’s going to eat less grass and produce less milk just because she’s worth less on paper?

Of course not. She’ll produce the same amount of milk tomorrow as she did yesterday. The money still flows in for the farmer.

It’s the same with a well-constructed income portfolio. If the share market crashes, do you think Australians will stop buying groceries, disconnect their power, close their bank accounts, and cancel their phone plans? They won’t. The companies paying you dividends are still selling their products. The income keeps flowing.

The tail doesn’t wag the dog.

This is why investors with beef cattle strategies panic when markets drop — they need to sell, and now they’re selling at exactly the wrong time. Investors with dairy cow strategies can sit back, collect their milk, and wait for the beef price to recover.

The only way to plan properly for retirement is to build an asset base that spins off plenty of cash without relying on markets going up.

Here’s where it gets really interesting.

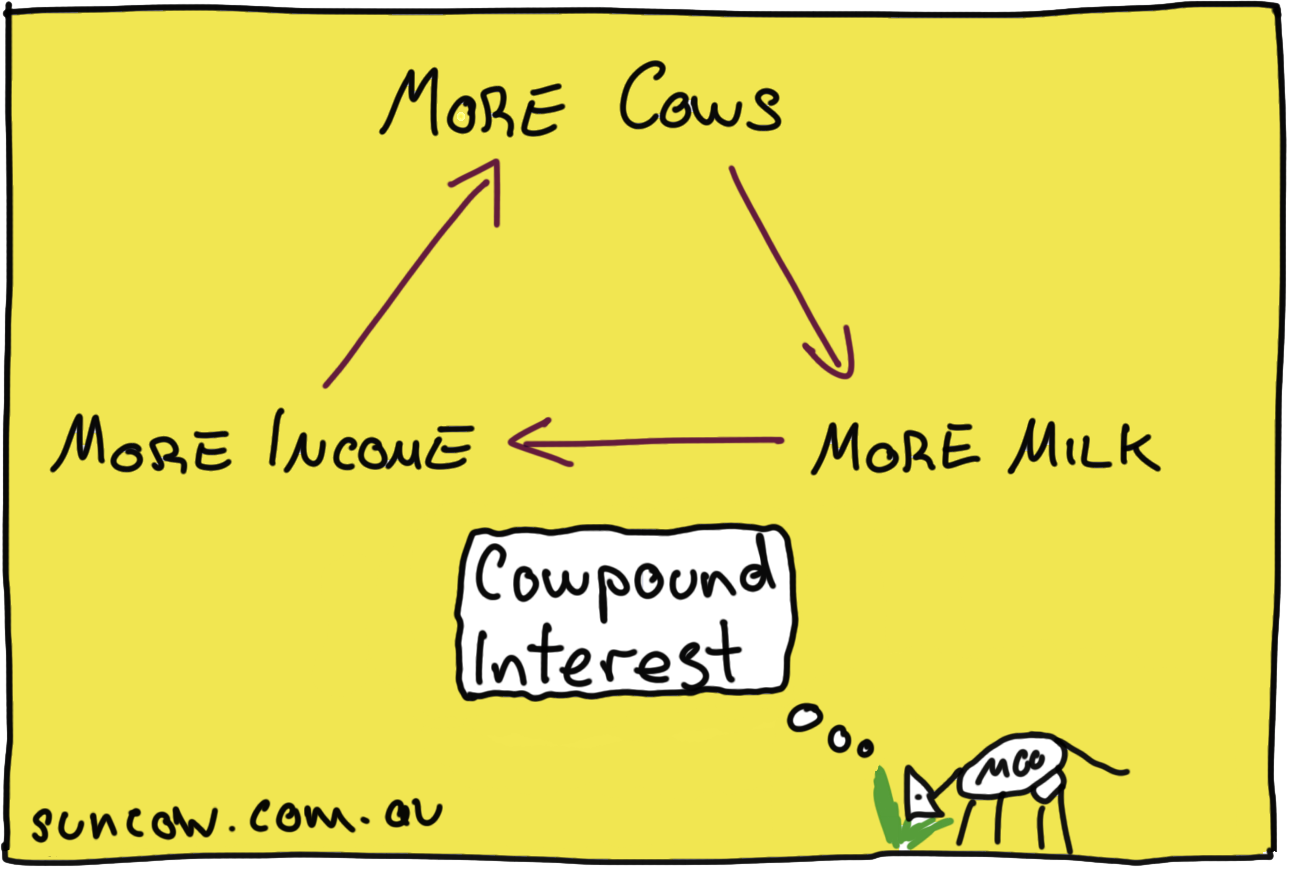

Let’s imagine your super is just a tax-effective paddock. The only thing that matters is what type of cows you put in it.

If you fill your paddock with dairy cows, and all you do is sell the milk to buy more dairy cows — your herd gets bigger. A bigger herd produces more milk. More milk buys more cows. And then it grows again. More milk, more cows, more income.

At Suncow, we call that cowpound interest. It’s the retirement income equivalent of compound interest — and it’s the most powerful wealth-building mechanism available to Australian investors, particularly inside super.

The beauty of it is its simplicity. You don’t need to pick the right stock. You don’t need to time the market. You don’t need to make clever tactical decisions. You just need to keep growing your dairy herd until it’s time to retire — and then live off the milk.

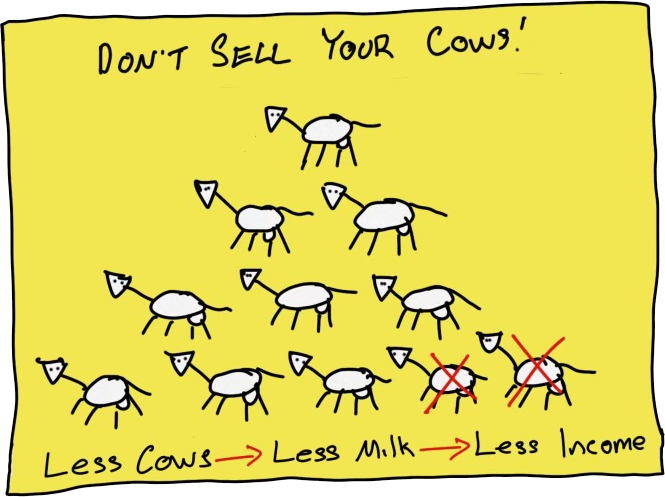

And whatever you do: don’t sell your cows to fund your retirement. Fewer cows means less milk means less income. It sounds obvious when you put it that way. But it’s exactly what conventional retirement advice tells people to do.

Most investors are attracted to beef cattle because they love watching their investments appreciate in value. An investment that goes from $10 to $20 feels like winning. It feels like wealth.

But here’s the irony: eventually, dairy cows become more valuable than beef cattle — because of their production capacity.

It’s the difference between the goose and the golden egg.

The beef investor wants to breed the biggest, fattest goose possible so he can sell it. The dairy investor looks after her goose and lives off the golden eggs indefinitely.

Beef investors buy and sell. Dairy investors buy and hold.

One strategy requires perfect timing and constant activity. The other requires patience and a good herd.

Guess which one sleeps better at night.

The 2 Cows Strategy isn’t abstract. In practical terms, your dairy cow portfolio is built from income-producing assets — things that pay you regularly just for owning them.

In an Australian retirement context, this typically includes:

Australia’s franking credit system makes dividend investing here uniquely powerful. For retirees in a low or zero tax environment — which most self-funded retirees are — fully franked dividends from Australian companies can be extraordinarily tax-efficient. In some cases, excess franking credits are refunded in cash.

To illustrate how this comes together: a couple in Balmain, both 62, with combined super of $850,000 and a $75,000 income target might structure their retirement income like this:

Total: ~$75,000 per year. Without selling a single cow.

That’s the system working. And it keeps working whether markets go up, down, or sideways — because none of it depends on selling anything.

Growth investing makes sense when you have decades on your side. But arriving at retirement with a predominantly growth-focused portfolio means your income depends on selling — which puts you at the mercy of whatever market exists when you need the money. The transition from beef to dairy needs to start earlier than most people think, and it needs to be deliberate.

Not every high-dividend stock is a good dairy cow. Some companies pay elevated dividends because they’re distributing capital rather than genuine earnings — there’s no real milk, just the illusion of it. Sustainable, growing income from fundamentally sound businesses is what you’re after. Quality matters as much as yield.

Money is like soap: the more you handle it, the less you have. Every trade, switch, tactical tweak and “quick move” chips away at your wealth through fees, spreads, capital gains tax, and timing mistakes. The dairy cow approach works because you milk the cows consistently — not because you’re constantly rearranging the herd. Buy and hold isn’t lazy. It’s the strategy.

Many Australians with moderate super balances assume they’ll never qualify for the Age Pension. This is an expensive assumption. The taper rates mean that many clients who’ve never thought of themselves as pension-eligible qualify for a meaningful part-pension — often $10,000–$20,000 per year — particularly after legitimate asset structuring. A dairy cow you’ve forgotten you own is still producing milk. You just can’t see it yet.

“We thought we’d need $1.2 million to retire. Adam showed us how we could retire comfortably on $680,000 by optimising our Age Pension and using our home equity strategically. Getting a clear answer changed everything.” — Matt & Sarah, Balmain

“At 58, I was panicking about having only $320,000 in super. The One Page Plan gave me a clear path to retire at 65 with confidence. I finally knew exactly what I needed.” — Emma, Rozelle

“Adam’s advice helped us realise we could actually retire two years earlier than planned. We’ve never slept better.” — David & Helen, Balmain

Once you know your income number — not your balance, your income — FORO loses its power.

The One Page Financial Plan is the simplest way to get that clarity. One session. One page. Your retirement income target, where you stand today, and exactly what needs to happen to get you there.

Book Your One Page Financial Plan Today

No pressure. No jargon. No sales pitch.

📧 adam@suncow.com.au | 📞 0418 785 200

$660 inc GST | 100% satisfaction guarantee or you don’t pay.

The 2 Cows Strategy works best when the advice behind it is completely unconflicted.

Here’s the uncomfortable truth: advisers who earn commissions on financial products have a financial incentive to recommend those products. An adviser on trailing commissions from a growth-focused managed fund isn’t going to enthusiastically recommend you shift toward income-producing assets — even if that’s exactly what your retirement needs.

As a fee-for-service Balmain financial adviser, I don’t earn commissions. I don’t receive trailing fees. My only incentive is to give you advice that actually works — because my business runs on referrals and reputation, not product margins.

The 2 Cows Strategy gets recommended because it’s the right approach. Not because anyone’s paying me to say so.

Is the 2 Cows Strategy suitable if I have a smaller super balance?

Yes — and it’s actually more important with a smaller balance, because you can’t afford to rely on capital drawdown. Understanding how to maximise income from the Age Pension, smart asset structuring, and tax-efficient investing is especially valuable when every dollar counts.

Do I need to pick individual shares to build a dairy cow portfolio?

Not at all. Many clients build their entire income portfolio through managed funds, LICs, and ETFs — without ever picking a single stock. The principle is income focus, not stock picking.

What about capital growth — doesn't inflation erode my income over time?

The 2 Cows Strategy isn’t anti-growth. Beef cattle still have a role as the growth engine in a long retirement. The question is getting the right balance for your situation — enough dairy cows to fund your income needs, enough beef cattle to protect against inflation over 20–30 years. That’s exactly what the One Page Financial Plan maps out.

How is this different from what my super fund does by default?

Most default super fund options are growth-focused — beef cattle operations. They’re appropriate for accumulation. As you approach retirement, the question becomes whether your herd is shifting toward income production. Your super fund’s default strategy almost certainly isn’t doing that for you automatically.

What if I'm already retired — is it too late to apply this strategy?

Not at all. Many clients come to us already retired and restructure their portfolios toward income focus. The transition requires careful planning — particularly around tax and sequencing — but the underlying strategy is just as applicable.

You’ve spent decades building your herd. Now it’s time to find out whether it’s producing enough milk.

The One Page Financial Plan gives you that answer in a single session. Your numbers. Your income target. Your path.

📧 adam@suncow.com.au | 📞 0418 785 200

$660 inc GST | 100% satisfaction guarantee or you don’t pay.

Information provided by Suncow Wealth is general in nature and does not take into consideration your personal financial situation. It is for educational purposes only and does not constitute formal financial advice. Remember, the value of any investment can go down as well as up. Before acting, you should consider seeking independent personal financial advice that is tailored to your needs. Suncow Wealth Pty Ltd is a Corporate Representative No.441116 of AFSL 342766.