“Get out now!”

“…if you’re a struggling homeowner with some equity left in your property, you should get out while you can…”.

This blunt suggestion (paraphrased) came from NAB Chief, Ross McEwan last August.

And his reason was balance sheet simple. The NAB warned property prices could drop by 32% in a worst-case scenario by the end of 2022.

(Read. They most likely wanted to rid their loan book of wobbly loans before they started defaulting).

And then this happened last Saturday…

A free-standing, two-bedroom wreck in Crows Nest (NSW) sold for $900,000 above its ambitious reserve price of $2.1m. A whopping 43% above the reserve!

And if you think paying overs of $900k for a run-down shack is nuts, the stock market is worse! And mostly on borrowed money too.

Either way, we’re in another boom market, for now.

All thanks to rock bottom interest rates, relaxed responsible lending rules and first home buyer grants.

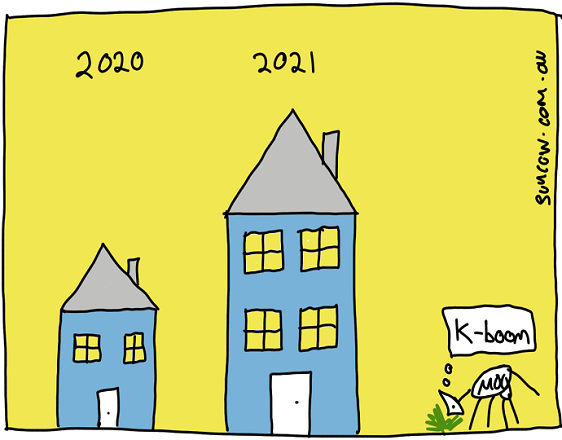

The problem is, we also have a ‘K’ shaped property market.

Meaning, when the economy was slammed into lock-down last year, a heap of renting millennials moved back in with their parents to reduce costs.

But by year end, a wave of them returned to the property market not as renters, but as home buyers.

Consequently, house prices have gone north while rents have gone south. Hence the ‘K’.

Not surprisingly, I now get emails from worried parents like this…

Hey Adam,

My kids have missed out. They’ve squirreled away every last dollar and just when they had enough saved up for a deposit, the market took off again. I’m worried they will never get a start especially if interest rates stay low for at least three years. What should they do?

Short answer: don’t panic!

In the words of the world’s greatest investor, Warren Buffett…

When other’s get greedy, I get scared. But when others get scared, I get greedy.

Cheap money and irrational behaviour are driving every market to manic heights at the moment – stocks, property, commodities, cryptocurrencies, bonds, credit…. even lumber!

So here’s what I reckon you should do…

If you’ve missed the property market, keep saving. Your chance will come, it always does.

But if you’ve found a place you really, really, really want, then be prepared to live in it for at least 10 years because this craziness won’t last.

I’d also recommend a 20% deposit to avoid mortgage insurance and then hammer the mortgage while rates are low.

But if you’re looking for an investment property, I’d tattoo this to the inside of your eyelids:

i. It’s a renters market not a landlord’s market

ii. I wouldn’t touch any long-term investment with a yield (rent, dividends) less than 5% *.

(You can stop squirming about the tattoo now, I was joking!)

Finally, don’t bank on interest rates staying at ground zero for three years just because the Fed (US) or RBA said so.

Inflation could force up interest rates sooner than later due to excessive stimuli.

Never before has there been a bigger disconnect between asset prices and reality.

These are krazy times. A time to keep a kool head!

Have a great weekend!

Adam

* Doesn’t include capital gain, strictly rental and dividend income only. This means most residential properties don’t cut the grade.

Back paddock – if Facebook was a nation, it would be the third largest nation in the world by population.

Still Going In — But Not Forever At some point, usually somewhere between 55 and 65, a thought surfaces that you can’t quite ignore. You’re not ready to stop completely. But you’re not sure you want to keep going at full pace either. The commute that felt fine at 45 feels heavier at 58. The …

Continue reading “Transition to Retirement: An Inner West Guide”

This question comes up constantly with clients in their 50s, and understandably so. The kids are largely through school. The income is better than it’s ever been. And for the first time in years, there’s actually surplus cash at the end of the month. The question is where to put it. The mortgage-vs-super debate gets …

Continue reading “Should You Pay Off Your Mortgage or Boost Your Super?”

The decade before retirement is the most financially consequential of your life. The decisions you make between 55 and 65 — or 50 and 60, depending on when you plan to stop working — have an outsized impact on what the next 30 years look like. Get them right and you arrive at retirement with …

Information provided by Suncow Wealth is general in nature and does not take into consideration your personal financial situation. It is for educational purposes only and does not constitute formal financial advice. Remember, the value of any investment can go down as well as up. Before acting, you should consider seeking independent personal financial advice that is tailored to your needs. Suncow Wealth Pty Ltd is a Corporate Representative No.441116 of AFSL 342766.