You’re lying awake at 2am again, running the numbers in your head. Your super balance. Your age. That retirement date you’ve been circling on the calendar.

You’ve Googled “how much do I need to retire” about 50 times this month. But every article gives you a different answer.

Some say $500,000. Others insist on $1.2 million.

And you’re sitting there thinking: “Which one is right? Do I have enough? Should I work another five years? Am I completely deluding myself?”

Here’s what nobody tells you: You’re asking the wrong question.

Every financial website, super fund calculator, and well-meaning mate at the pub has an opinion about how much you need to retire. They love throwing around big, scary numbers.

$1 million. $1.5 million. $2 million if you want to “be safe.”

But here’s what drives me crazy about all this retirement advice: asking “How much super do I need to retire?” is like a farmer obsessing over the value of his cows instead of focusing on how much milk they produce.

Big retirement numbers feed your ego, income feeds your belly.

Retirement confidence comes from reliable income, not a magic lump sum.

Instead of fixating on a lump sum figure, here’s what actually matters:

How much income will you need each year to live the life you want?

That’s it.

Because retirement isn’t about having a massive balance. It’s about generating enough reliable income to pay for the life you’ve been working towards.

You can’t spend your super balance at the butcher in Balmain. You can’t pay your electricity bill with your house equity. You can’t take your grandkids to Taronga Zoo with your share portfolio value.

What you need is income. Regular, reliable, sufficient income.

That’s it.

Because retirement isn’t about having a massive balance. It’s about generating enough reliable income to pay for the life you’ve been working towards.

Think about it:

What you need is income. Regular, reliable, sufficient income.

That 2am anxiety you have? That’s FORO – the Fear of Running Out.

And it’s keeping thousands of Balmain pre-retirees awake at night, even when they have plenty saved.

The problem isn’t your super balance. The problem is not knowing whether it’ll generate enough income to last. Once you know your income number, FORO loses its power.

And that changes everything about how we plan your retirement.

Your straight-talking Balmain financial planner who believes retirement planning should be simple, not scary. I help locals like you figure out the income you actually need, not some generic number from the internet.

In This Guide:

Stop losing sleep over retirement “what-ifs.”

Get the clarity you crave with a One Page Financial Plan – the simplest way to discover your true retirement number and eliminate FORO forever.

No pressure. No jargon. No sales pitch.

Just an honest conversation about your retirement goals and what it will take to fund the lifestyle you want.

To book:

📧 Email: adam@suncow.com.au

📞 Call: 0418 785 200 if you prefer to chat

$660 inc GST | 100% satisfaction guarantee or you don’t pay.

The Association of Superannuation Funds of Australia (ASFA) suggests:

Single person: $51,000 annually for a comfortable retirement

Couple: $72,000 annually for a comfortable retirement

But effective retirement planning goes beyond these averages. What you actually need depends on:

When determining your retirement target, consider:

A Balmain financial planner considers all potential retirement income:

Living in Balmain gives you unique retirement advantages:

Most financial plans are dense 50-page reports that end up in a drawer.

Our One Page Financial Plan answers your two most important questions – how much do I need and will I have enough. Period.

No jargon. No confusion. Just clarity on whether you’re on track or what needs to shift.

You’re smart with money. You’ve built a career, paid down your mortgage, saved into super for decades. But when you think about retirement, something doesn’t feel right.

Here’s what I’ve noticed after helping hundreds of Balmain and Inner West locals plan their retirement: The smartest people often make the same four mistakes.

The good news? They’re all fixable once you know what to look for.

You fixate on hitting $1 million in super, but that number tells you nothing about what you can actually afford to spend. What matters is how much income your assets will generate each year – not what they’re worth on paper.

Money is like soap: the more you handle it, the less you have. Every switch, trade, tweak and “quick move” chips away at your wealth through timing mistakes, fees, spreads and tax.

The traditional approach – build up capital, then gradually sell it down – is terrifying and precarious. One market crash forces you to sell assets at depressed prices, shortening your retirement timeline dramatically.

Most retirees know their super balance but have no idea what their life really costs. Without understanding your true spending — not guessing, not “should be fine” numbers — you can’t build a reliable retirement income plan. The danger? Either living too tightly for no reason… or overspending and running into trouble later.

Here’s something most financial planners won’t tell you: your total super balance matters far less than how that money works for you.

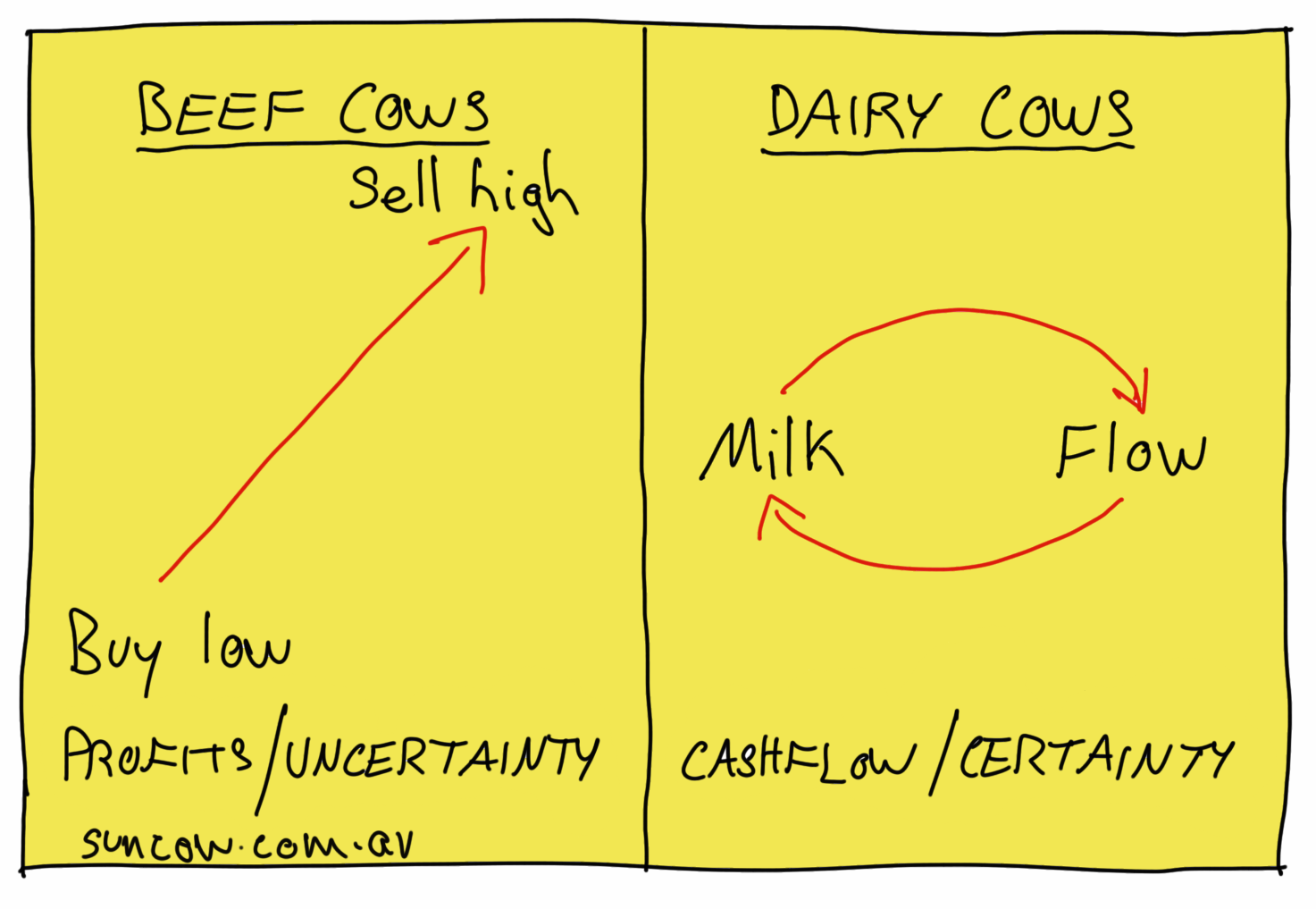

Think of your retirement assets like a farm. Some assets are like dairy cows — they produce regular income through dividends, rent, or interest. Others are like beef cattle — they grow in value but don’t produce anything until you sell them.

Most Australians obsess over the total size of their herd (their super balance) when what really matters is how many dairy cows they have producing reliable income each year.

This is what I call the “2 Cows Strategy,” and it completely changes how you approach retirement planning. Instead of asking “how much do I have?”, you ask “how much income does this generate?”

A $600,000 super balance with the right mix of income-producing assets can deliver more reliable retirement income than $800,000 in growth-only investments.

“We thought we’d need $1.2 million to retire. Adam showed us how we could retire comfortably on $680,000 by optimizing our Age Pension and using our home equity strategically. Getting a clear answer changed everything.” — Matt & Sarah, Balmain

“At 58, I was panicking about having only $320,000 in super. The One Page Plan gave me a clear path to retire at 65 with confidence. I finally knew exactly what I needed.” — Emma, Rozelle (near Balmain)

“Adam’s advice helped us realize we could actually retire two years earlier than planned. We’ve never slept better. Having a local Balmain financial planner who understands our situation made all the difference.” —David & Helen, Balmain

Stop losing sleep over retirement “what-ifs.”

Get the clarity you crave with a One Page Financial Plan – the simplest way to discover your true retirement number and eliminate FORO forever.

No pressure. No jargon. No sales pitch.

Just an honest conversation about your retirement goals and what it will take to fund the lifestyle you want.

To book:

📧 Email: adam@suncow.com.au

📞 Call: 0418 785 200 if you prefer to chat

$660 inc GST | 100% satisfaction guarantee or you don’t pay.

No commissions. No product sales. No conflicts of interest. Just advice that’s genuinely in your best interests. As your Balmain financial planner, my only focus is helping you get accurate answers.

Know exactly what you’re paying upfront. No hidden fees or ongoing charges unless you choose ongoing support.

I understand the Inner West property market, lifestyle costs, and opportunities available to Balmain residents. This local expertise is essential because costs and opportunities vary significantly across Sydney. As a local Balmain financial planner, I’ve seen firsthand how location affects retirement needs.

Over 500 One Page Financial Plans completed with a 100% satisfaction guarantee. Every client receives the same thorough, personalized approach.

I only have $200,000 in super. Can I still retire comfortably?

Yes. With the Age Pension providing a foundation and smart asset structuring, many clients retire comfortably with less super than they expected. The key is understanding what you need based on your specific situation, not generic assumptions.

What if I want to retire before 67?

Early retirement requires specialized planning strategies. There are approaches for accessing income before Age Pension eligibility, though they require more planning. We can show you exactly what’s possible and help determine your early retirement target. As a Balmain financial planner, I’ve helped several clients achieve early retirement.

Should I pay off my mortgage before retiring?

It depends. Sometimes keeping the mortgage and investing the difference creates better outcomes. We’ll model both scenarios for you and show how each affects your retirement income.

How much does the One Page Financial Plan cost?

$660 including GST. 100% satisfaction guarantee or you don’t pay.

What happens after I get my plan?

We can discuss ongoing support options if you prefer professional implementation. Your relationship with me can be as ongoing or as limited as you prefer. There are no lock-ins.

Do you only work with wealthy clients?

Not at all. Our services are designed for everyday Australians with super balances between $100,000 and $1 million. Many clients are surprised to learn their target is more achievable than they thought, regardless of their starting point. As a Balmain financial planner, I work with people from all financial backgrounds.

Stop losing sleep over retirement “what-ifs.” Get the clarity you crave with a One Page Financial Plan – the simplest way to discover your true retirement number and eliminate FORO.

No pressure, no sales pitch — just an honest conversation about your retirement goals.

To book:

📧 Email: adam@suncow.com.au

📞 Call: 0418 785 200 if you’d rather speak directly.

$660 inc GST | 100% satisfaction guarantee or you don’t pay.

Information provided by Suncow Wealth is general in nature and does not take into consideration your personal financial situation. It is for educational purposes only and does not constitute formal financial advice. Remember, the value of any investment can go down as well as up. Before acting, you should consider seeking independent personal financial advice that is tailored to your needs. Suncow Wealth Pty Ltd is a Corporate Representative No.441116 of AFSL 342766.