In the lead up to Christmas, two clients threatened to leave and find another adviser if I didn’t invest their money.

The pressure of FOMO (fear of missing out) was beginning to build and they insisted we hurry up and do something, anything!

One client tried goading me by admitting he and his wife were already speaking with another adviser who had some very good ideas for their money.

This was my reply…

Dear John and Jenny*,

As you’re aware, this is the most expensive market in history and to be honest, I would rather lose a client than invest their money at these levels.

Three days later we parted company and everything was transferred to their new adviser.

In the past two weeks, the markets have dropped 11 – 16%. The NASDAQ in particular, has lost nearly all the gains made during 2021 in less than a fortnight.

So what’s going on?

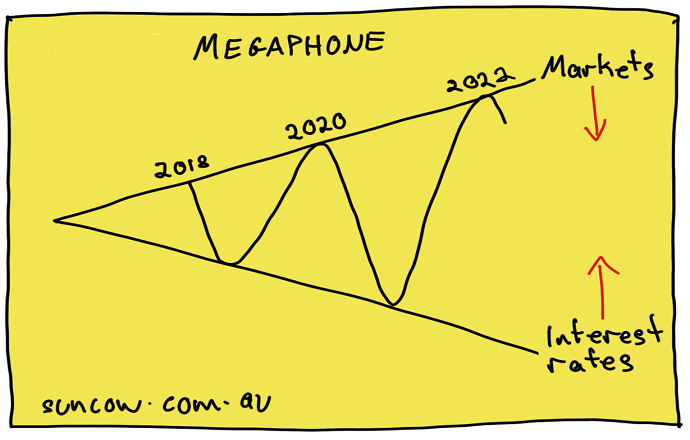

It’s simple. We are approaching the end of a ‘megaphone cycle’.

It works like this…

Interest rates have been in a cutting cycle since the Global Financial Crisis (GFC) to help resuscitate and stimulate world economies.

And every time rates have been cut, asset prices have gone higher creating a divergence between the two, like a ‘megaphone’.

Make sense?

Ironically, this megaphone cycle would have finished two years ago when asset prices were already over extended but then Covid reared its invisible head.

At the time, it looked like the whole world was going to hell in a hand basket and so the central banks cut rates to zero and this accentuated the megaphone cycle further.

But now this cycle is coming to an end because inflation has rocketed and the only way of tempering it is to hike interest rates.

The problem is, the RBA and Federal Reserve spent the whole of 2020-21 assuring us rates wouldn’t rise until 2024. However, they never expected inflation to go this high either.

This megaphone cycle will end like a nasty marriage break-up. There will be lots of volatility (separation) before it finally corrects (divorce).

Have a great weekend!

Adam

* not their real names

Still Going In — But Not Forever At some point, usually somewhere between 55 and 65, a thought surfaces that you can’t quite ignore. You’re not ready to stop completely. But you’re not sure you want to keep going at full pace either. The commute that felt fine at 45 feels heavier at 58. The …

Continue reading “Transition to Retirement: An Inner West Guide”

This question comes up constantly with clients in their 50s, and understandably so. The kids are largely through school. The income is better than it’s ever been. And for the first time in years, there’s actually surplus cash at the end of the month. The question is where to put it. The mortgage-vs-super debate gets …

Continue reading “Should You Pay Off Your Mortgage or Boost Your Super?”

The decade before retirement is the most financially consequential of your life. The decisions you make between 55 and 65 — or 50 and 60, depending on when you plan to stop working — have an outsized impact on what the next 30 years look like. Get them right and you arrive at retirement with …

Information provided by Suncow Wealth is general in nature and does not take into consideration your personal financial situation. It is for educational purposes only and does not constitute formal financial advice. Remember, the value of any investment can go down as well as up. Before acting, you should consider seeking independent personal financial advice that is tailored to your needs. Suncow Wealth Pty Ltd is a Corporate Representative No.441116 of AFSL 342766.