Politicians refer to it as, ‘putting the rubbish out’.

Meaning, if a negative media release has to go out, it’s usually done on a Friday evening when most people are at the local boozer and not watching the news.

This Moowsletter isn’t devious but you’ll probably wish you didn’t see it.

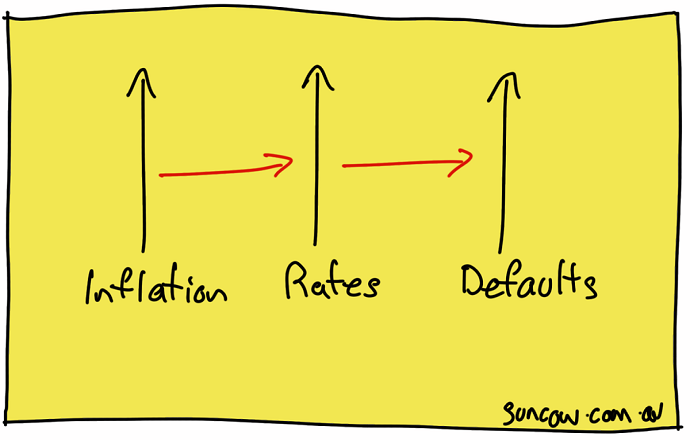

Since interest rates went up on Tuesday, some within the commentariat have suggested a heap of people will be in trouble if rates go to 2.5% by the end of the year.

So, will it really be that bad?

Maybe, but only if you believed the cardigans at the Reserve Bank who said rates wouldn’t go up until 2024.

Make no mistake, Reserve Bank boss Phillip Lowe should be impeached for luring borrowers into thinking rates would remain lower for longer. It was never, ever, going to happen and it’s a disgrace he even suggested it.

In any case, let’s put a few things into perspective.

Firstly, only one third of the property market have a mortgage, while another third have their house paid off, and the other third rent.

Therefore, the only group I’m concerned about are those who got sucked in by FOMO (fear of missing out) during 2021.

You were warned! Manic markets never last.

The big winners out of this will be the wannabe buyers who stared FOMO in the face but didn’t yield to it.

They’re now on the sidelines enjoying some JOMO – the joy of missing out.

Fortunately, the JOMOs are sitting on a heap of cash so they’ll eventually put a floor underneath this market, but not before it drops, possibly back to pre-pandemic levels.

I wouldn’t say the property market is doomed, but I would definitely say some buyers are.

Specifically, I’m talking about the ones who believed money would remain cheap for years to come and that anything with a roof on it never goes down in value.

That’s the good rubbish out of the way. #councilcleanup

Here’s the bad rubbish…

Right now, approximately one-fifth of the 3,000 largest publicly traded companies in the US are considered ‘zombie firms’ because they’re not making enough money to cover their interest expenses. [1]

That’s 600 of the largest 3,000 companies who are in the mud.

It’s akin to living off your credit card but you don’t have enough money to make the minimum monthly repayments.

Unfortunately, the Fed’s recent interest rate hikes, and record inflation, may be enough to push a wave of these companies from zombie to cemetery.

Which immediately raises two more questions…

Who are the lenders financing these businesses?

And who are their suppliers (and soon to be creditors)?

Fortunately, most of the loans for these firms come from the junk bond market which means the banks shouldn’t have too much exposure.

However, their suppliers which include other listed companies, could get knocked around a bit.

When I first spoke about inflation and interest rates in March 2021, I was criticized for being too negative. And maybe I was.

Well guess what?

There’s more.

We’re now heading into the final phase of the post-pandemic bubble, defaults.

And if my read is right, we’ll need a whopping big dumpster to clean up the mess.

Have a great weekend!

Adam

[1] Bloomberg.

Back paddock: when things go wrong, don’t go with it – Glenn Stearns, founder of Stearns Lending and cancer survivor.

It’s a Tuesday morning in March 2020. You check your super balance before breakfast. It’s down $80,000 from last week. You’re supposed to retire in four months. Your coffee goes cold on the bench. This is the scenario that terrifies every pre-retiree in Balmain. Not the abstract idea of a market crash – but the …

Continue reading “What Happens to Your Income When the Stock Market Crashes?”

You’re 52. You check your super balance: $380,000. Your stomach drops. “That’s all? After 30 years of working?” Then you remember that article you read: “You need $1 million to retire.” Quick math: You need to more than double your super in 13 years. That seems… impossible. So you do what many Australians in their …

Continue reading “Building Your Financial Herd: Investment Strategy in Your 50s”

Imagine you inherit a dairy farm with 50 healthy cows. Each cow produces milk that you can sell for income. Together, they generate enough money to live on comfortably. Now imagine someone suggests: “Why don’t you sell five cows this year to buy a new truck?” Sure, you’d get the truck. But now you only …

Continue reading “Why Your Investment ‘Cows’ Should Never Be Sold in Retirement”

Information provided by Suncow Wealth is general in nature and does not take into consideration your personal financial situation. It is for educational purposes only and does not constitute formal financial advice. Remember, the value of any investment can go down as well as up. Before acting, you should consider seeking independent personal financial advice that is tailored to your needs. Suncow Wealth Pty Ltd is a Corporate Representative No.441116 of AFSL 342766.