This time four years ago the bushfires had just started to rip through the east coast of Australia like a massive fireball, decimating everything in its path.

Six weeks later, the clouds opened up and broke one of the worst droughts in history.

Green shoots appeared everywhere and sale yards were full of shouting farmers bidding against each other, desperate to re-stock their farms.

Consequently, protein prices took off – lamb, beef, chicken, pork, dairy, the lot.

Food prices jumped just before Covid reared it’s invisible head and commodity prices kept soaring until late 2022.

But now they’ve done a massive U-turn. The sheep and cattle economies have collapsed.

Weather forecasters are predicting an El Nino drought and farmers can’t off-load their stock fast enough.

Consequently, sheep and cattle prices have plummeted 80-90% from their recent highs.

Take for example my mate Ted. Last week he sent 425 sheep to the Forbes sales yards and netted $5,935 after costs (freight, agents fees, etc.)

This time last year he would have clipped $40,000 for the same sheep. That’s an 85% drop in 12 months.

Imagine trying to fight inflation and service a loan with a drop in income like that!

So by now you’re probably thinking…why hasn’t the cost of beef and lamb dropped for consumers as well farmers?

It’s simple. Pricing power.

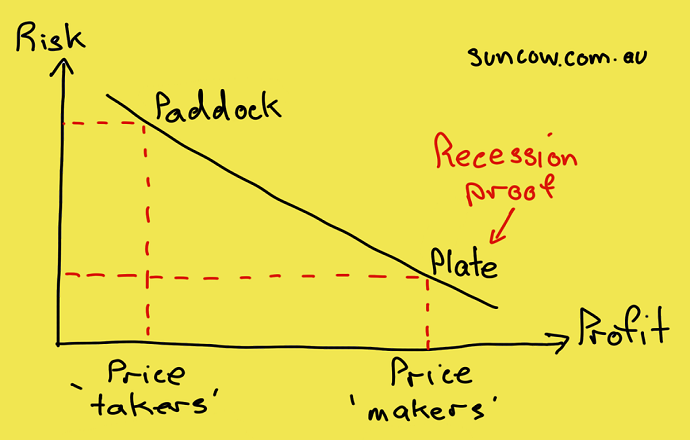

Primary producers are ‘price takers’ while the big retailers are ‘price makers’.

Primary producers operate high risk, low margin (profit) businesses while retailers such as Coles and Woolies operate low risk, high margin businesses.

Price makers can increase their prices asymmetrically because they sell non-discretionary items which we consume on a daily basis – food, energy, telecommunications, banking, etc.

i.e. products essential to our survival.

Price makers also know how much pain their customers can tolerate before they shop elsewhere.

As a result, price makers are very polarizing. Consumers despise them as much as shareholders love them because of their ability to make you put your hand in your pocket, every month.

Businesses which sit at the consumption end of the food chain generally make the best investments. They’re both inflation and recession proof.

The problem is they’re too expensive to buy at the moment.

But that may change.

As a general rule, but not always, stock prices follow commodity prices and commodity prices follow weather patterns.

Have a great weekend!

Adam

Back paddock – if you went back to school what subject would you give more attention to?

Still Going In — But Not Forever At some point, usually somewhere between 55 and 65, a thought surfaces that you can’t quite ignore. You’re not ready to stop completely. But you’re not sure you want to keep going at full pace either. The commute that felt fine at 45 feels heavier at 58. The …

Continue reading “Transition to Retirement: An Inner West Guide”

This question comes up constantly with clients in their 50s, and understandably so. The kids are largely through school. The income is better than it’s ever been. And for the first time in years, there’s actually surplus cash at the end of the month. The question is where to put it. The mortgage-vs-super debate gets …

Continue reading “Should You Pay Off Your Mortgage or Boost Your Super?”

The decade before retirement is the most financially consequential of your life. The decisions you make between 55 and 65 — or 50 and 60, depending on when you plan to stop working — have an outsized impact on what the next 30 years look like. Get them right and you arrive at retirement with …

Information provided by Suncow Wealth is general in nature and does not take into consideration your personal financial situation. It is for educational purposes only and does not constitute formal financial advice. Remember, the value of any investment can go down as well as up. Before acting, you should consider seeking independent personal financial advice that is tailored to your needs. Suncow Wealth Pty Ltd is a Corporate Representative No.441116 of AFSL 342766.