“You stupid cow. Get back in your paddock and stay there!”

This a redacted email minus the ‘f’ bombs I received from a bloke in March last year.

And if he was trying to throw me it didn’t go close. I copped much worse before the last federal election when I rallied for franking credits.

Back then, being called a cow was a good day!

So why did this bloke got a bit bristly with me?

In March last year, I produced a video for my clients and somehow, he got a copy of it.

Specifically, I opined inflation would scream and interest rates would go up much sooner than 2024…despite every assurance from the Fed and RBA that they wouldn’t.

And that’s when this bloke got a bit hot under the brisket.

Not only did he vehemently disagree (as was his right), but he also wanted proof because he reckoned no one else was talking about this stuff.

Which wasn’t true.

Most people just didn’t want to hear it back then because crypto, property and stocks were going gang-busters.

Any talk of inflation or a rate hike was like a wet dog walking into your lounge room.

Get out!

So I referred him back to the video which clearly showed why interest rates would go up well before 2024…

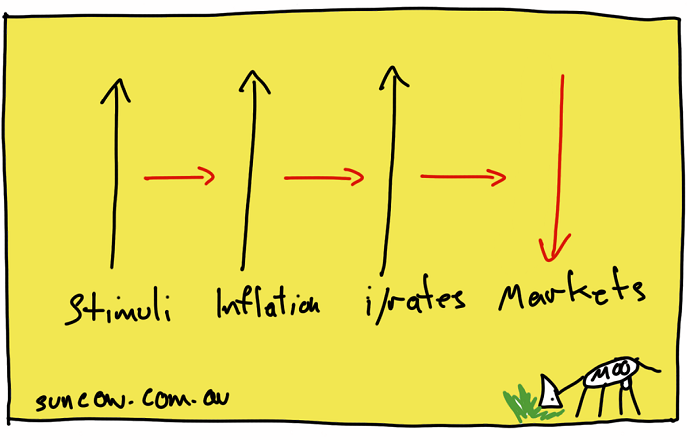

Firstly, every developed economy was awash with cash thanks to all the stimuli that had been injected by governments and central banks during the pandemic.

This meant most consumers were enjoying increased spending power which was putting upward pressure on energy, food and asset prices in particular.

Hello inflation!

Consequently, 10-year bonds, which are a proxy for interest rates, began moving from 0.5% in August 2020 back to their pre pandemic levels of 3% as of last week.

Hello interest rates!

Put simply, red flags started appearing before Christmas 2020 while everyone was drooling over Bitcoin.

But this was…and still is…my biggest concern.

Not since the Great Depression, has there been a bigger divergence between the rich and poor thanks to the pandemic.

The pandemic has made the rich wealthier, while the poor have gone backwards rapidly, both financially and socially.

Pensioners are falling behind because food, rent, insurance, gas, and power prices have rocketed while their incomes have remained fixed.

These people are financially choking.

But its borrowers who will feel the heat most going forward because this week inflation hit a twenty year high of 5.3%. It blew all expectations out of the water.

Inflation normally oscillates around 2%.

And according to Bill Evans, the Westpac chief economist, this means the RBA cash rate will go from 0.1% to 1.5% before Christmas…this year!

Meaning, if you’ve borrowed at 2%, your mortgage rate will go to approximately 3.5%. In dollar terms, if your interest payment is $1,000pm, it will go to around $1,700pm.

I don’t know what paddock this cow was supposed to go back to last March but this I know for sure; the paddock I’ve been standing in for the past eighteen months has been screaming inflation!

And thats why interest rates are about to charge like a fiery young bull…further and faster than expected.

Happy grazing!

Adam

Back paddock – a person with good health has a thousand dreams, a person who doesn’t has one dream.

Still Going In — But Not Forever At some point, usually somewhere between 55 and 65, a thought surfaces that you can’t quite ignore. You’re not ready to stop completely. But you’re not sure you want to keep going at full pace either. The commute that felt fine at 45 feels heavier at 58. The …

Continue reading “Transition to Retirement: An Inner West Guide”

This question comes up constantly with clients in their 50s, and understandably so. The kids are largely through school. The income is better than it’s ever been. And for the first time in years, there’s actually surplus cash at the end of the month. The question is where to put it. The mortgage-vs-super debate gets …

Continue reading “Should You Pay Off Your Mortgage or Boost Your Super?”

The decade before retirement is the most financially consequential of your life. The decisions you make between 55 and 65 — or 50 and 60, depending on when you plan to stop working — have an outsized impact on what the next 30 years look like. Get them right and you arrive at retirement with …

Information provided by Suncow Wealth is general in nature and does not take into consideration your personal financial situation. It is for educational purposes only and does not constitute formal financial advice. Remember, the value of any investment can go down as well as up. Before acting, you should consider seeking independent personal financial advice that is tailored to your needs. Suncow Wealth Pty Ltd is a Corporate Representative No.441116 of AFSL 342766.