Little did I know October 2019 would be my last country trip for at least a year, maybe more.

Back then, there were only two things I was certain about.

The drought was so bad some farmers couldn’t afford to keep their dogs, and the stock market was over-cooked and due for a correction.

And the only thing I remember more than the scorched paddocks were some of the wrestles I had with a few clients.

I wanted a few of them to take some money off the table because I was expecting another GFC. The problem was, our Cashcow portfolio was yielding 8 to 10% after tax (not including capital gain).

Understandably some clients didn’t want to lighten their holdings.

My other concern was we were already in an aggressive cutting cycle (interest rates) which meant lower profits for the banks and therefore a cut in dividends.

Bottom line…I was expecting a correction of 30 to 40%, minimum.

And then Corona reared its invisible head and the market dropped 38% in five weeks over February and March.

(Lesson: the catalyst for a correction is often the thing you least expect. If it’s overpriced, it will correct regardless).

At one stage, things were so bleak it felt like the whole world was heading to hell in a handbasket.

Consequently, the RBA slashed interest rates from 1.5% to 0.1%. A 90% cut!

Subsequently, the stock market rocketed and went from depressed to manic mostly fueled by cheap money and stimulus cheques.

And now we find ourselves in the same place as October 2019. Only higher.

The US markets (S&P 500 and NASDAQ) are 18% and 36% higher (respectively) than their pre-COVID highs.

So will it last? NO!

Here’s why.

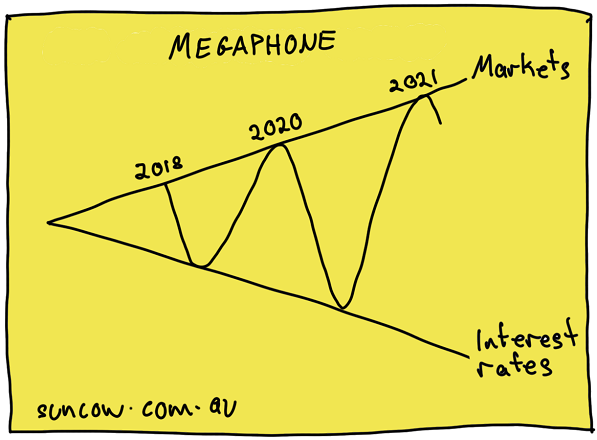

For the past three years the stock market has been creating a ‘megaphone’ price pattern…thanks to interest rates.

It works like this. Each time the economy has weakened and the market has dropped, central banks have cut rates which has forced the stock market to rally up and create a new high.

The problem is it also works in reverse. Meaning, each time the market makes a new high and is overpriced, it corrects into a deeper low thanks to a weaker economy.

Hence the ‘Megaphone Effect’.

The good news is, the Megaphone Effect is very rare. The bad news is, I think we have one more correction to go and it could possibly be our biggest yet.

Put simply, too much stimuli has been pumped into the economy and its overheating the markets…stocks, property, commodities, cryptocurrencies, the lot.

But the biggest risk of all is inflation which means interest rates may go up sooner than expected and that would definitely be the end of the Megaphone Effect.

However, I think the markets will correct before that happens.

Just make sure you’re standing near the door when the music stops.

Have a great weekend!

Adam

Back paddock – what the wise perosn does in the beginning, the fool does in the end. Charlie Munger

It’s a Tuesday morning in March 2020. You check your super balance before breakfast. It’s down $80,000 from last week. You’re supposed to retire in four months. Your coffee goes cold on the bench. This is the scenario that terrifies every pre-retiree in Balmain. Not the abstract idea of a market crash – but the …

Continue reading “What Happens to Your Income When the Stock Market Crashes?”

You’re 52. You check your super balance: $380,000. Your stomach drops. “That’s all? After 30 years of working?” Then you remember that article you read: “You need $1 million to retire.” Quick math: You need to more than double your super in 13 years. That seems… impossible. So you do what many Australians in their …

Continue reading “Building Your Financial Herd: Investment Strategy in Your 50s”

Imagine you inherit a dairy farm with 50 healthy cows. Each cow produces milk that you can sell for income. Together, they generate enough money to live on comfortably. Now imagine someone suggests: “Why don’t you sell five cows this year to buy a new truck?” Sure, you’d get the truck. But now you only …

Continue reading “Why Your Investment ‘Cows’ Should Never Be Sold in Retirement”

Information provided by Suncow Wealth is general in nature and does not take into consideration your personal financial situation. It is for educational purposes only and does not constitute formal financial advice. Remember, the value of any investment can go down as well as up. Before acting, you should consider seeking independent personal financial advice that is tailored to your needs. Suncow Wealth Pty Ltd is a Corporate Representative No.441116 of AFSL 342766.