Here’s a quick quiz for you.

If you invested $1 in gold 100 years ago, how much do you think it would be worth today?

A. $3

B. $300

C. $3,000

D. $30,000

You ready?

The answer is A. $3

You’re probably shocked, right?

Especially since gold and silver have so much integrity thanks to people’s association with it. e.g. wedding rings

So what drives the price of gold?

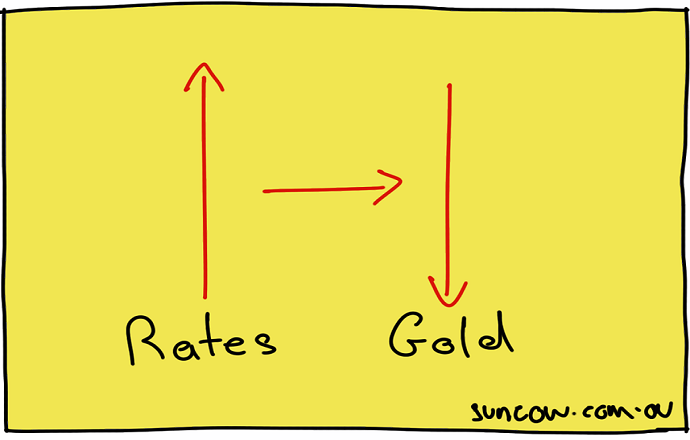

Interest rates. Period.

Gold is a proxy for interest rates. Meaning, when interest rates go down the value of gold goes up, and vice versa.

The last cutting cycle is proof positive.

Between 2017 and 2020, rates were slashed from 2.5% to 0.1%, and gold rocketed from $1,200 to an all-time high of $2,000 an ounce, during the same period.

In other words, as the value of money depreciates (low rates) the value of gold appreciates.

However, the common belief is gold goes up when the stock market tanks because investors go in search of a safe haven such as gold.

Hmmm, not quite.

For example, I’ve experienced three stock market corrections during my career (2000, 2008, 2020) and not once has a client ever rung me during a correction and said, “BUY GOLD!”

People always go to cash when things get a bit hairy.

But if you believe gold is a stock market hedge, why isn’t gold trending up right now while the stock market is trending down?

Again, interest rates.

Gold has dropped nearly 30% since March (more than the stock market) amid fears of higher inflation and more rate cuts.

Put simply, interest rates in the US are tipped to hit 4% by the end of the year. [1]

But there’s a curve ball…

Recession.

If rates go too high too soon, they could easily tip the economy into a recession. And the signs seem ominous we’re heading in that direction.

And if that occurs, then there’s a chance rates will be cut again to help kick start the economy.

And if rates are cut, gold will start heading up again.

Here’s my point…

Gold doesn’t climb like stocks and property.

Instead it cycles like a washing machine. Just like interest rates.

And that’s why $1 invested in gold 100 years ago is only worth $3 today.

Have a great weekend!

Adam

[1] Bloomberg

Back paddock – when someone constantly says, “I don’t know”, it usually means…“I know but I don’t want to say anything.”

It’s a Tuesday morning in March 2020. You check your super balance before breakfast. It’s down $80,000 from last week. You’re supposed to retire in four months. Your coffee goes cold on the bench. This is the scenario that terrifies every pre-retiree in Balmain. Not the abstract idea of a market crash – but the …

Continue reading “What Happens to Your Income When the Stock Market Crashes?”

You’re 52. You check your super balance: $380,000. Your stomach drops. “That’s all? After 30 years of working?” Then you remember that article you read: “You need $1 million to retire.” Quick math: You need to more than double your super in 13 years. That seems… impossible. So you do what many Australians in their …

Continue reading “Building Your Financial Herd: Investment Strategy in Your 50s”

Imagine you inherit a dairy farm with 50 healthy cows. Each cow produces milk that you can sell for income. Together, they generate enough money to live on comfortably. Now imagine someone suggests: “Why don’t you sell five cows this year to buy a new truck?” Sure, you’d get the truck. But now you only …

Continue reading “Why Your Investment ‘Cows’ Should Never Be Sold in Retirement”

Information provided by Suncow Wealth is general in nature and does not take into consideration your personal financial situation. It is for educational purposes only and does not constitute formal financial advice. Remember, the value of any investment can go down as well as up. Before acting, you should consider seeking independent personal financial advice that is tailored to your needs. Suncow Wealth Pty Ltd is a Corporate Representative No.441116 of AFSL 342766.