Steve thinks I live in a cave…

“…I just read last week’s Moowsletter on your website…there’s no way interest rates are going up in the next three years…don’t you watch the news…get out of your cave!”

“Hi Steve, I’m tipping you’ve borrowed a lot of money?”

Steve must have been pretty fired up because he didn’t even have a dig at me about my ‘artwork’. Everyone else usually does!

Look, to be fair, Steve and the rest of his house bound mates may be right.

But there’s no way I’m telling clients everything’s sweet for the next three years just because the RBA or the (US) Fed said so.

Here’s why.

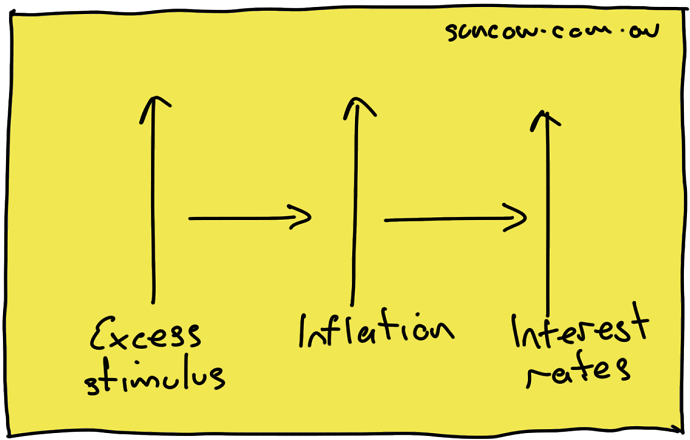

For the past twelve months every central bank around the world has printed and pumped squillions into their economies hoping to pull them out of a deep, dark hole.

And to an extent, it’s worked.

But everything has a tipping point and there’s now a growing concern they may have gone too far.

Put simply, the threat of inflation is gathering momentum and the only way to temper it is to either cut stimulus or hike interest rates.

So what do you do?

Do you sacrifice the poor and turn off the printing presses, or do you print more money at the risk of overheating the economy and force up interest rates?

Naturally, you’d keep printing and look after the poor.

But even if you continue with more stimulus, the poor may be no better off because their cost of living will simultaneously increase due to inflation.

Therefore, the net effect of more stimuli could be zero for those who need it most.

The problem is, concerns about an interest rate hike are also gathering momentum.

Enter the bond market…

Hang on Suncow! What’s a bond?

A bond is just a loan. And the only difference between a bond and a traditional loan is the lender of a bond is usually an investor. e.g. superfunds or private investors like you and I.

Make sense?

And this is where it gets interesting…

In the last five months, 10-year bond yields have gone from 0.5% to a recent high of 1.61%.

Meaning, investors (lenders) are now demanding higher interest rates from borrowers to compensate for inflation risk.

Or to put it another way, investors (lenders) expect the future cashflows of their repayments to diminish in value due to inflation, so they increase the interest repayments to compensate.

And eventually, central banks may be forced to do the same thing.

Meaning, they will eventually increase rates to protect consumers from a blow-out in living costs (inflation). Especially the poor.

The ‘lower for longer’ interest rate narrative may have worked during COVID, but the world is quickly moving on, and up.

Vaccines are re-opening economies with stacks of cash and pent-up demand.

And if 10-year bond yields are a forerunner for interest rates, you can expect a rate rise sooner than later.

The writing is on the cave wall.

Have a great weekend!

Adam

Back paddock – a mate of mine keeps a book of funny comments made by his son who has just turned five. On Thursday evening he phoned me with this gem…

“Hey Dad, I just worked out how to make a baby. You need a female and an email!”

It’s a Tuesday morning in March 2020. You check your super balance before breakfast. It’s down $80,000 from last week. You’re supposed to retire in four months. Your coffee goes cold on the bench. This is the scenario that terrifies every pre-retiree in Balmain. Not the abstract idea of a market crash – but the …

Continue reading “What Happens to Your Income When the Stock Market Crashes?”

You’re 52. You check your super balance: $380,000. Your stomach drops. “That’s all? After 30 years of working?” Then you remember that article you read: “You need $1 million to retire.” Quick math: You need to more than double your super in 13 years. That seems… impossible. So you do what many Australians in their …

Continue reading “Building Your Financial Herd: Investment Strategy in Your 50s”

Imagine you inherit a dairy farm with 50 healthy cows. Each cow produces milk that you can sell for income. Together, they generate enough money to live on comfortably. Now imagine someone suggests: “Why don’t you sell five cows this year to buy a new truck?” Sure, you’d get the truck. But now you only …

Continue reading “Why Your Investment ‘Cows’ Should Never Be Sold in Retirement”

Information provided by Suncow Wealth is general in nature and does not take into consideration your personal financial situation. It is for educational purposes only and does not constitute formal financial advice. Remember, the value of any investment can go down as well as up. Before acting, you should consider seeking independent personal financial advice that is tailored to your needs. Suncow Wealth Pty Ltd is a Corporate Representative No.441116 of AFSL 342766.